6 digital banking challenges you should know about (and how to turn them into opportunities)

Here are the most pressing digital banking challenges that traditional institutions face. And, perhaps even more importantly, the practical steps you can take to turn each one into a growth and new revenue opportunity.

1. Why legacy infrastructure slows digital transformation

Many banks still rely on outdated legacy systems that are expensive and complex to modernise or integrate with new cloud and AI technologies, making even minor updates nearly impossible.

This limits their ability to offer agile, innovative services and compete with fintech firms.

An additional challenge is that migrating to modern systems while maintaining service continuity can be complex and costly.

How to overcome legacy system challenges in digital banking

75% of banks still struggle to implement new solutions due to legacy infrastructure, but those adopting cloud-native APIs see faster innovation and lower operational risk.

Banks should adopt API-first designs, breaking legacy monoliths into modular, interoperable units.

As a result, this enables integration of new functionality without full system replacement, significantly speeding time-to-market for new products and features.

This modular approach integrates old and new systems, while maintaining service continuity.

Migration to cloud infrastructure brings scalability, real-time processing, and cost savings.

Modern cloud platforms enable the rapid launch of new services, providing disaster recovery, operational agility, and enhanced compliance and security features.

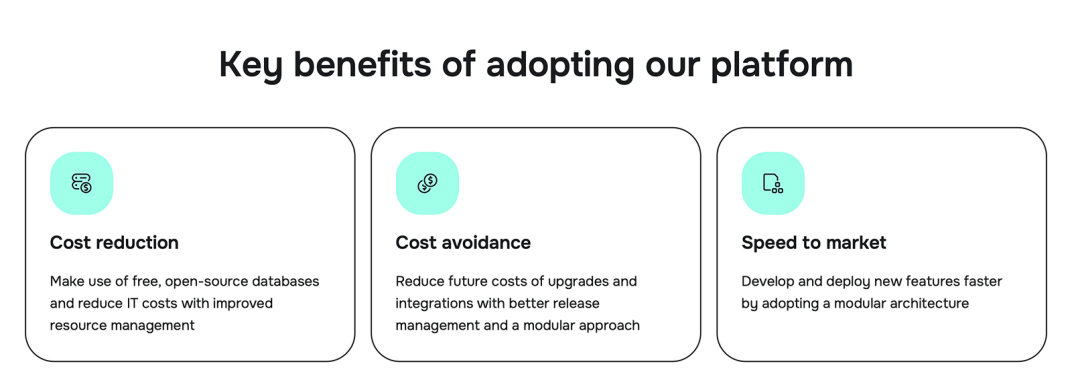

How Meniga helps banks modernise without disruption

Meniga provides flexible, scalable solutions that work smoothly with your existing systems, helping modernise your digital environment, no matter what technology you use.

Micro-services fluency uses modular solutions that interact via APIs, enabling you to:

-

Implement new features rapidly,

-

Respond to market trends swiftly, and

-

Scale-specific digital banking capabilities as needed.

We support portability, which means you can move software and data seamlessly between on-premise and cloud environments (especially valuable for institutions transitioning gradually to cloud-native solutions).

Meniga delivers advanced system observability with continuous monitoring that detects issues before they impact users, ensuring banks can scale their digital services while maintaining peak performance.

In addition, the use of free, open-source databases and improved resource management significantly lowers IT costs.

2. How to use AI to address Data Management challenges in digital banking

While AI is a key to personalisation, fraud detection, and automation, many banks struggle due to a lack of a clear AI strategy, data silos, and insufficient infrastructure. Talent for AI and cybersecurity is also in short supply, making it harder to build and maintain advanced solutions in-house.

Without addressing these gaps, you risk falling behind fintechs and digital-first competitors that can move faster and adapt more easily.

How to overcome AI and data management challenges in digital banking

Consider investing in unified data platforms that break down silos by integrating customer information across multiple channels and departments.

That way, you’ll get a 360-degree customer view, allowing you to deliver more personalised and consistent services.

These platforms offer near real-time analytics, quick fraud detection, fast credit scoring, and dynamic risk assessments.

After investing in data management, you can implement AI chatbots or virtual assistants to streamline your operations more efficiently.

AI chatbots and virtual assistants can:

-

Handle customer queries,

-

Automate back-office tasks,

-

Offer personalised product recommendations, and

-

Provide financial guidance around the clock.

Additionally, since they are built on modern data lakes and cloud-based infrastructure, they also provide the scalable storage and processing power you’ll need for advanced AI algorithms.

How Meniga enables AI-driven Data Management and Personalisation

Meniga’s Enrichment Engine aggregates, consolidates, and enriches internal and open banking data to give you a 360-degree view of your customers’ spending habits and finances.

It turns raw data into a clear, visual story of your customers’ spending habits, with detailed merchant descriptions and categories, enabling you to better understand and cater to your customers.

As a result, you can tailor products, recommendations and services to your customers’ unique needs and spending patterns.

On top of that, it helps customers understand and optimise their ongoing payments, promoting better financial management.

3. Customer experience: the human side of digital banking challenges

Expectations for fast, personalised, and seamless mobile experiences continue to rise.

Customers compare their banking apps not just to other financial institutions, but to the best digital experiences in retail, travel, and entertainment.

They want interfaces that feel intuitive from the very first tap, backed by robust security measures that protect their data without creating friction.

At the same time, human support remains non-negotiable.

Customers expect knowledgeable assistance to be available at any time, through chat, phone, or video.

When apps feel clunky, slow, or outdated compared to leading consumer technology, satisfaction decreases, and can lead to churn.

For banks, closing this experience gap is becoming a defining factor in retaining and growing their digital customer base.

How to overcome customer experience challenges in digital banking

Delivering an exceptional mobile experience starts with human-centric design.

It means apps that are intuitive to navigate, easy to customise, and built around the way customers actually bank.

Layered with AI-powered personalisation, these apps can:

-

Provide personalised financial tools to help people boost their financial health,

-

Recommend the right financial products at the right time,

-

Detect suspicious activities, and

-

Provide fast, accurate support through intelligent chatbots.

By combining this digital efficiency with omnichannel support, including human-assisted services, you can offer the best of both worlds: the convenience customers expect and the personal connection that builds long-term loyalty.

How Meniga helps banks deliver next-level experiences

Our AI-powered Insights help you leverage data to anticipate customer needs and create proactive communication strategies.

Thus, you can:

-

Become a trusted financial advisor by truly getting to know your customer and providing helpful advice.

-

Nudge customers towards banking solutions they will use and benefit from, increasing the ROI of existing features.

-

Increase digital sales by promoting relevant products to the right customers, at the right time.

-

Analyse behavioural data to create ultra-specific customer segments, such as Likely to Invest or Starting a Family

-

Leverage real-time events from any external or internal banking tool to ensure timely delivery.

-

Provide the perfect omni-channel experience by delivering to any channel via own systems, CRM platforms, or others.

For the real-world impact, you can check our case study on how Meniga helped UniCredit prioritise customer experience through Digital Banking.

4. Increased competition: neobanks and fintech redefine digital banking challenges

The rise of digital-only banks and non-banking fintech players has intensified competition.

They operate without the constraints of legacy systems, enabling them to launch new features and services at remarkable speed.

Customers, especially younger generations, are comfortable switching providers in search of better experiences, more competitive rates, and innovative features.

This ‘shifting’ loyalty puts significant pressure on traditional banks to accelerate their own innovation cycles and modernise their offerings.

Fintech startups and neobanks innovate at a great speed, offering services that sometimes bypass traditional banking systems.

For example, they introduce alternative payment systems, decentralised finance solutions, and new ways to manage money that challenge the very role of conventional banks.

How to overcome competition challenges in digital banking

For traditional banks, staying relevant means matching this pace of change while leveraging their trusted brand and customer relationships as competitive strengths.

One idea to achieve that is to adopt a hybrid approach combining technology and human expertise.

By adopting agile methodologies, banks can accelerate product development and roll out new features at speed, refining them through continuous customer feedback.

Building strong ecosystem partnerships with fintechs, technology vendors, and even industry competitors can expand capabilities, improve operational efficiency, and enrich the customer experience.

At the same time, focusing on niche and highly personalised offerings allows banks to stand out.

Leveraging deeper AI-driven insights will enable you to provide tailored solutions while reinforcing trust and delivering exceptional customer service.

It can help you maintain a competitive advantage against purely digital challengers.

How Meniga helps banks stay competitive

With Meniga’s neobank-grade tools and solutions, you can boost customer retention with engaging and habit-forming experiences.

Besides Enrichment and Insights, we provide a multi-award-winning PFM Suite to help your customers understand their finances and create healthy financial habits for prolonged engagement.

You can:

-

Provide a clear and accessible overview of each transaction, including category, merchant details, and spending history.

-

Group transactions into categories using simple tags or comments.

-

Incorporate intuitive budgeting features that enable spending goals on a global, category, or sub-category level.

-

Automatic budgeting based on a customer’s spending history.

-

Enable customers to track and manage all cards, accounts, and transactions from any source with a Google-like search.

5. Regulatory compliance: one of the toughest digital banking challenges

Banks face growing regulatory burdens, including data privacy, know your customer (KYC) rules, anti-money laundering (AML), and ESG reporting.

Regulatory fragmentation worldwide increases compliance complexity and cost.

Other challenging aspects include identity verification and monitoring suspicious transactions with fewer false positives.

How to overcome compliance challenges in digital banking

Automation and scalable compliance solutions are the key to staying ahead of evolving rules while reducing operational burden.

By implementing advanced RegTech tools, banks can use AI-powered screening, transaction monitoring, and automated reporting to streamline processes and improve accuracy.

Also, embed privacy controls into system architectures and customer interfaces from the start.

Staying informed about worldwide requirements, conducting regular audits, and maintaining transparency in data handling will help achieve global regulatory alignment.

How Meniga supports regulatory compliance

Meniga supports both Payment Initiation Services (PIS) and Account Information Services (AIS), making it fully compliant with PSD2 and Open Banking regulations.

Meniga is also fully certified under ISO27001, the leading international standard for information security management.

Therefore, banks are safe to integrate with our flexible APIs while maintaining compliance with strict data protection and consent requirements.

It’s this modular API framework that enables banks to adapt quickly to evolving regulations without rebuilding core systems.

Moreover, our Enrichment capabilities reduce risks related to data quality.

Thus, we support regulatory reporting requirements by ensuring data consistency and completeness.

By providing accurate, enriched, and well-organised transactional data combined with analytics, we help banks prepare for audits and regulatory reporting demands efficiently.

6. Cybersecurity and fraud: the most pressing digital banking challenge

With increasing digital transactions, cyberattacks remain the top operational risk. Banks are prime targets for cyberattacks due to the sensitive nature of financial data.

They must comply with strict data privacy regulations, such as GDPR and CCPA, while protecting against increasing threats.

Fragmented regulatory environments across countries also complicate coordinated security measures.

How to overcome cybersecurity and fraud challenges in digital banking

Strengthening cybersecurity in banking requires a multi-layered approach that combines advanced technology and strict controls:

-

AI-driven real-time threat detection: Use AI and machine learning to continuously monitor for unusual behaviours, detect cyberattacks instantly, and trigger automated responses before damage occurs.

-

Zero trust security architecture: Apply a “never trust, always verify” model with continuous authentication and strict identity management to reduce access-related risks.

-

Cloud security enhancements: Protect cloud-hosted applications and data with encryption, multi-factor authentication (MFA), continuous monitoring, and Cloud Security Posture Management (CSPM) tools.

-

Vendor security management: Conduct in-depth risk assessments, enforce tight access controls, and continuously monitor third-party vendors to guard against supply chain attacks.

-

Regular penetration testing and vulnerability management: Use ethical hacking simulations and automated scanning tools to detect and fix vulnerabilities before they can be exploited.

-

Employee training programs: Provide ongoing cybersecurity awareness training to reduce human error risks, such as phishing and social engineering attacks.

-

Incident response and backup: Maintain tested incident response plans and segmented backups to ensure rapid recovery from breaches.

When combined, these strategies safeguard sensitive data but also protect customer trust, arguably the most valuable asset for any bank.

How Meniga strengthens fraud detection

Meniga uses machine learning models to analyse transaction amounts, frequency, geographic location, and user behaviour to proactively flag suspicious activities.

The continuous learning capability means the system adapts to evolving fraud tactics, providing faster and more accurate detection.

By enriching transaction data into clear, categorised spending insights, Meniga increases transparency and enables better anomaly detection.

In return, this helps banks detect fraud faster and reduce false positives, improving both security and customer experience.

Combining AI with rule-based systems enhances the capability to detect complex and emerging threats.

Thus, the system can generate real-time alerts for suspicious activities, empowering banks to act quickly before fraud impacts customers.