European regulations and competition is reducing revenue which banks get from payments and other banking services. Rewards marketing offers a new way to bridge the gap.

Increased competition and innovation

Perhaps the best known regulation which impacts revenues from payments is the European Payment Services Directive or PSD2. This directive came into effect in the beginning of this year. It enables new players to compete with banks for payment services and account information. These are known as Payment Initiation Service Providers (PISPs) and Account Information Service Providers (AISP). The purpose of the regulation is to increase competition and innovation in this area.

The EU Regulation on cross-border payments and the Single Euro Payments Area (SEPA) is also negatively impacting banking revenues from payments. Banks must charge the same for cross-border payments in euros within the European Economic Area as they charge for euro payments within a country. The regulation also applies to Swedish kronor.

Coffeeshop leads the way

Increased competition and technical innovation in payments is not restricted to Europe. In the United States, Starbucks has taken the lead in mobile payments, leapfrogging not only banks but also technology giants such as Apple, Google and Samsung. Starbucks supports both Android and Apple devices so the cross platform approach is clearly paying off for them. The customer value generated with great user interface and rewards is, however, the most important factors for the success Starbucks is enjoying.

Low risk revenue under threat

As somebody who has worked for a bank providing online banking services to government and businesses, I appreciate that financial institutions like relatively low risk revenue from services and transactions. But in a digital world where competition from new market entrants and regulators are restricting the ability of banks to charge for these kind of services, there is a need to bridge an emerging revenue gap for banks.

Build ecosystems for banking growth

In their ´Global banking outlook 2018´ report, EY warns that ´many banks will struggle to keep up in an innovation arms race. Further, the risk of getting big bets on new technologies wrong is high, and failure will prove costly. As such, banks need to do more to embrace the shift from innovating in a silo to participating in an innovative ecosystem and collaborating with partners and peers.’

Building new revenue generating eco systems

Enter rewards marketing. This is where customers get cashbacks, for accepting brand funded offers. Retailers or merchants not only get access to customers, it is also fairly straightforward to attribute transactions to campaigns. As any marketing or sales director will know that is important to understand return on investment for campaigns.

Rewards enables brands and merchants to build loyalty, increase their share of wallet or introduce themselves to new customers. Cost of campaigns is offset by low promotional costs. Merchants and retailers only pay commission to on sales that take place.

Customers will want to to stay with a bank that enables them to save money. Especially when they are able to pay less for goods of services which are tailored to their needs. It is a win win situation all around. Rewards places banks at the center of a revenue generating eco system of smart customers and savvy brands, retailers and merchants.

New revenue sources for banks

We at Meniga believe that banks are in a unique position to benefit from rewards marketing. Revenue is generated from commissions of sales realised through marketing campaigns and sales of anonymized marketing reports to brands which show in detail how they stand vis-a-vis their competitors for important customer segments.

Our experience of rewards

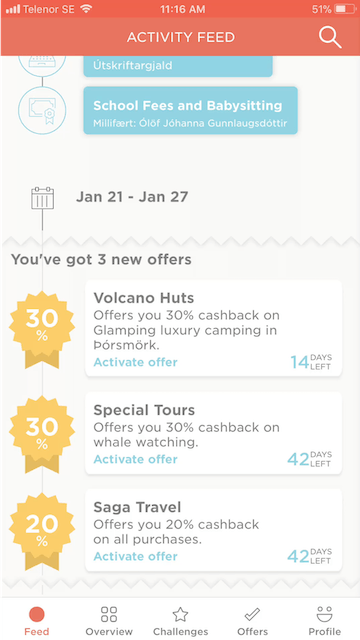

In Iceland, we at Meniga are involved in two rewards marketing programs. Firstly, we run a program with our partners at Íslandsbanki bank. Their rewards program contains cashback offers from a wide range of brands and is available to customers through the Íslandsbanki app. Secondly, we run our own personal financial management mobile and web apps. The personalised offers from brands help to build engagement and enrich the social media like feed in our app and web site.

How does our Merchant Portal work?

We give brands which participate in the program access to a web based interface where they can manage their campaigns. We use advanced segmentation algorithms to analyse customer transaction history, Personal Finance Management (PFM) engagement data, CRM information, demographics and other customer data to help brands deliver highly personalised and relevant offers to customers.

Brands tap into the Meniga app user base with personalised offers which are redeemed by getting a cash back for purchases.

Merchants can see the effectiveness of their campaigns in the portal with detailed but anomysed reports.

We continue to develop our rewards marketing features based on the feedback we get from our engaged user base and innovative banks which use our solution to revintent their value proposition. Watch this space!