Building Positive Financial Habits

First part in a four post series about meaningful engagement in digital banking

Banks are not just competing with banks any more. Tech giants and household names such as Google, Amazon, Facebook, Apple and WeChat are placing themselves between banks and their customers by providing financial actions and insight. Banks are now competing with user experience powerhouses for the top of mind ranking and the go-to place for financial activities.

The most common starting point for social media players entering financial services are mobile payments and peer-to-peer money transfers. For example, users of mobile messaging service Snapchat can now send money to each other via its Snapcash feature. Their success has given them the confidence to move into digital banking — Facebook and Google are offering similar features and Apple’s move into mobile payments is well documented.

The idea of social media players providing financial services is something consumers are open to.

Nearly three quarters of Millennials say they are more interested in new financial offerings from the likes of Google, Amazon and Apple than from their own traditional bank, according to The Millennial Disruption Index.

It’s no coincidence either that big businesses are making their move now. From 2018, the new European Payment Services Directive (PSD2) will give third-party providers access to banking customers’ account data. This provides opportunities for non-banking rivals to gain traction in financial management and payment services apps on the back of bank data.

Banks have realised that the smartphone is rapidly becoming the main gateway to their customer base, and they find themselves in the race to become one of those 4–5 apps that people use every day. They also find that they are competing with players that are much better at engaging people digitally than they are. Superior user experience has perhaps been somewhat of a nice to have for many banks, but is now becoming a clear competitive advantage.

So, what should banks do?

Banks are under pressure to dramatically improve their digital customer experience and incremental improvements won’t get you far. The good news is that they still have a competitive edge — most notably due to access to customers and financial data at scale. However, with PSD2 around the corner, this advantage is slowly eroding, so the time to utilise it is now.

Getting it right is essential — developing sustainable high-quality engagement is far from easy. The vast majority of smartphone apps fail to deliver long-term engagement. Often we get requests from banks seeking a gamified approach to financial management. But the buzz around Pokémon Go is mostly over and many of the Angry Birds have flown. We feel that you need a different approach.

Banks should learn from past successes and failures and in our view the key to sustainable engagement in digital banking is to focus on what we call meaningful engagement.

Building positive financial habits

The first step to meaningful engagement is to help people develop positive financial habits. If you can leave customers thinking: “This was good use of my time” after every session, then you are onto something.

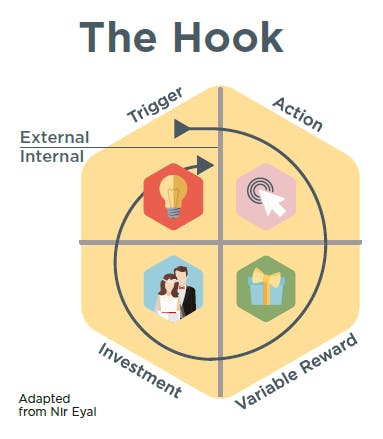

Many successful businesses use the Nir Eyal Hook Model to create habit-forming loops — using triggers and consecutive hook cycles to develop new habits. This is a good starting point to develop increased engagement, but you need to be careful in using this approach as you don’t want to end up as a bad habit. All the churn without valuable rewards can quickly lead to a drop in engagement.

To drive longer term meaningful engagement, the focus must be on habits that drive real value and impact — again, you need to designing for time well spent.

Valuable rewards can come in the form of world class usability — for example, by removing hurdles for common tasks like checking balance and transferring funds.

Positive impact on people’s lives is another example of a valuable reward. Fitness and wellbeing apps such as Strava, Headspace and Fitbit, are good sources of inspiration for how to drive engagement in developing positive habits. Rather than taking 10,000 steps a day, people could for instance set a target of saving 10% of their income each month. Similarly, Meniga’s Challenges module, a new financial fitness offering, suggests personalised spending goals, such as a 10-day challenge to spend less money on fast food, to help people reach their savings targets in small attainable increments. Focus on one area of spending for a short period of time. It helps you keep motivated and hopefully change your spending habits for good.

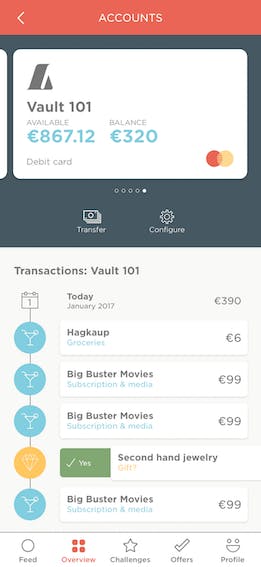

Sometimes, positive habits can be built out of the simplest of features. When Meniga launched its latest B2C app in Iceland, we optimised the user experience around engaging customers in transaction categorisation.

If there is uncertainty about how a transactions should be categorised, we prompt our users to tell us what category best fits the transaction — suggesting what we believe is the most likely option. This way, we created a habit by asking people to confirm uncertain categories and re-categorising when necessary using actionable colour and swipe actions. This resulted in more than 60% of the monthly active user base being engaged in categorisation — investing in making the product work better for them and increasing their spending awareness at the same time. We have even received comments from highly motivated users complaining about too few categorisation confirmations. It just goes to show, if you give consumers some purpose to their engagement, they are more than happy to oblige.

Categorisation is one example of a habit loop where triggers prompt investment from the user in the form of confirming or changing the category. The reward is that the system leans and reports become more accurate.

One last example is around education. If you teach me something that improves my life, I will forever be grateful.

Two years ago we decided to redesign the transaction detail page on our mobile app. Most banking apps provide little inspiration when you click on transactions. It is usually a mixed list of bank codes and meta data of little relevance to people.

We decided to bring in some of the insights and reports related to the transaction and give people information about how much they have spent at this particular merchant and category. Previously you had to drill down in separate reports to find this information. The short story is that after launching the new and enriched transaction detail screen, we went from 3% to 30% of active users clicking on transactions.

People now spend on average 23 seconds on the transaction detail screen. This is just one example of a new engagement hook and a starting point for many other features within our app. We also get constant feedback from our community on how this screen is helping people rethink their spending behaviour.

When it comes to rewards — immediate, tangible impact work the best, which is why personalised and relevant card-linked offers have the potential of developing strong habits via cash-back rewards.

These are just a few examples of how banks can build positive financial habits in the context of digital banking. For further inspiration check out our Insight Paper : Meaningful Engagement in Digital Banking

For more information visit www.meniga.com