Digital disruption has been brewing in the financial services industry for some time. Global VC & PE investments in FinTech have surged from USD 1B globally in 2009 t0 >USD 20B in 2015, creating a wealth of agile, innovative competitors across the banking value chain — particularly in personal & SME banking, where the customer experience is a key driver of differentiation.

The GAFAs (Google, Amazon, Facebook & Apple) and the BATs (Baida, Alibaba, Tencent) are all engaged in one or more form of financial services and 73% of Millennials are more interested in new financial services offering from the likes of Google, Amazon & Apple than from their own nationwide bank.

So far, banks have gotten away with a “wait and see” attitude towards digital disruption, making only incremental changes to their IT infrastructures and digital customer experience. To date, the financial impact of FinTech companies on the banking industry has been limited— capturing less than 2% of the global revenue pool. Nevertheless, most analysts agree that this is set to accelerate substantially in the coming years. As an example, McKinsey estimates 60% of consumer finance profits to be at risk in the next 10 years.

Enter PSD2 : Regulated Disruption across Europe

The revised European Payment Services Directive (PSD2) is driving European banks to a defining moment in 2018. PSD2 signals a significant shift in the balance of power in European retail banking, opening the door to FinTech disruptors and setting the financial services industry on a journey towards open banking. Specifically, PSD2 aims to drive increased competition, innovation and transparency across European payments and account information markets by granting third-party providers (TPPs) regulated access to a customer’s online account data and payment initiation. With PSD2, the consumer decides who can access its data and authorise payments from its accounts.

Furthermore, banks will bear the cost of compliance with no room to shift costs to third party suppliers or consumers.

So — What is the So-What?

The death of banks has been predicted many times over the past few decades — Bill Gates famously noted that “we need banking, not banks” back in 1994. Yet, here we are 22 years later and people are still (by and large) banking with the very same banks.

Are we at the tipping point now? Certainly the pressure is mounting: FinTech investments continue to rise, we are experiencing rapid channel and technology transitions, GAFA/BAT activity in financial services is intensifying, Millennials are losing faith in traditional banking and regulators are taking action to facilitate broader competition. The signs are all there.

While bottom-line impact remains limited, as noted above, customer disintermediation is becoming a serious issue for banks. The provision of financial services is gradually becoming more fragmented, and PSD2 is likely to substantially accelerate this trend. For example, peer-to-peer money transfer is starting to take place where it is most convenient (e.g. in social media channels) and loans and credit facilities are being granted exactly when they are needed (e.g. at time of purchase). This means banks are starting to lose valuable customer touch-points. When brands like Google, Facebook, Amazon and Apple are getting between you and your customers — then it is time to pay attention. The good old “wait and see” approach won’t do much longer.

Banks need to embrace PSD2 as an Opportunity

As PSD2 draws closer, banks are beginning to plan for compliance. API level access to account data & payment initiation requires banks to rethink IT architecture. But viewing PSD2 as a compliance exercise only is a big mistake.

PSD2 offers commercial opportunities for all players in the financial services industry and banks must take advantage (see below). With all the noise about disruption and competitive threats, banks need to remember that they still have a competitive edge — most notably due to access to customers and financial data at scale. This advantage is slowly eroding, so the time to utilise it is now.

No matter what, PSD2 will be a significant investment for banks and it is important to make that investment count.

Let me highlight three distinct, but not mutually exclusive, opportunities that I think banks should be pursuing in advance of PSD2 hitting the market.

Opportunity 1: Build a Best-in-Class (Open) API Platform

PSD2 will enforce banks to provide API access to basic financial data and payment initiation — and third party providers are lining up to build new consumer facing products and services. While this development is a concern for banks, it is also an opportunity.

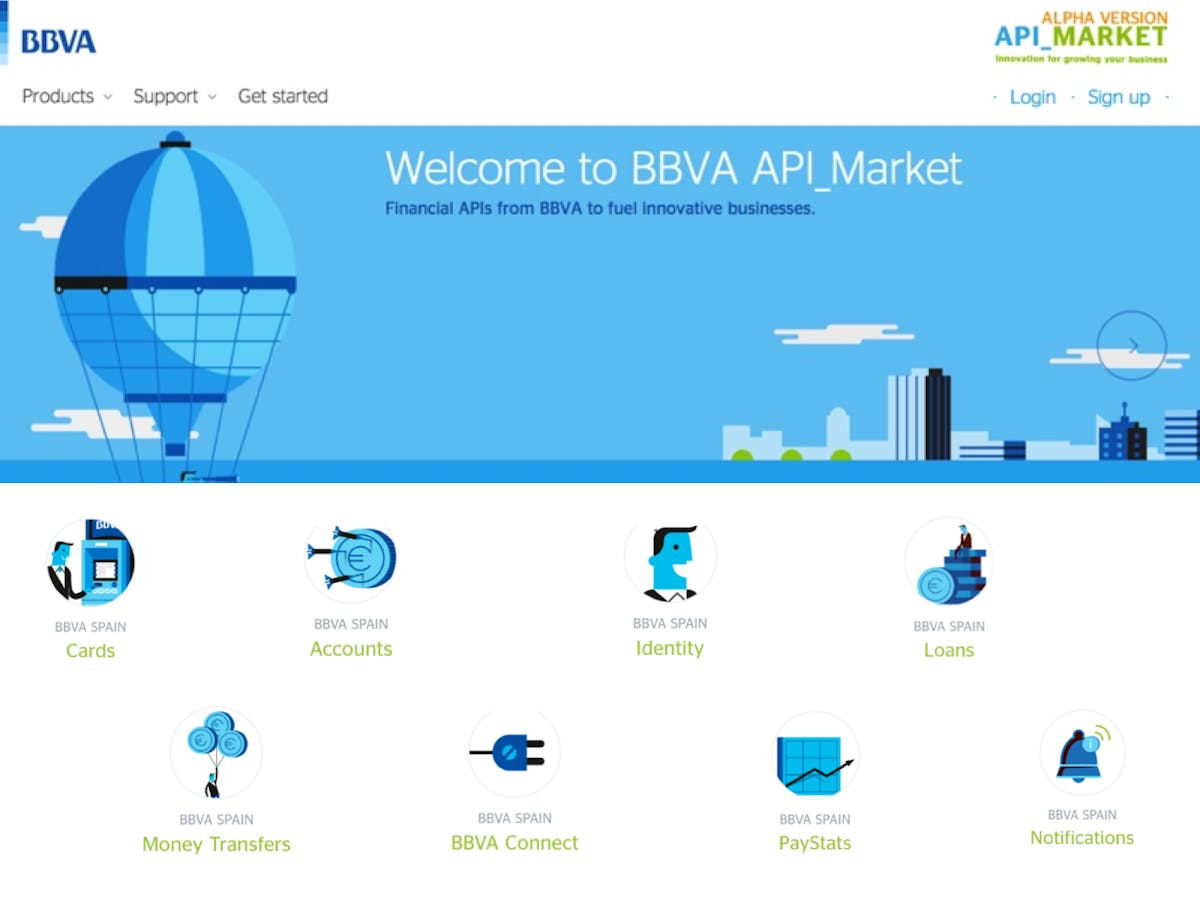

Building a best-in-class API platform means going beyond PSD2 requirements and build a personal finance data innovation platform with access to more data & functionality than just accounts, transactions & payment initiation. It means including standing orders, any type of financial products, customer profiles/demographic data, etc. It means enriching the data where possible — for example categorising & merchant mapping transactions. It means exposing the data through an API and develop a business model to monetise third party access via consumer consent. From a strategic point of view, the platform can be used in many ways. The data and functionality exposed by the platform can be fully open, open to select 3rd parties or used exclusively for internal innovation.

BBVA is a good example of a global bank that is already moving down this route. BBVA’s API Marketplace is out in alpha version with several interesting data feeds being used by select third party providers to develop new products and services for BBVA customers. The project, led by former Bank Simple co-founder and CFO Shamir Karkal, is highly visible inside and outside the bank.

Developing an open API platform does not necessarily equate to accepting the fate of exclusively becoming a back-end supplier of financial services. It should rather be seen as an extension to the business, much like Facebook, Google and Amazon have used it — a way to find more distribution for your products and services. For banks, this is about accepting that certain financial services are better supplied in context and outside the traditional digital banking channels — an inevitable trend they must adapt to. First movers can benefit from building strong (potentially exclusive) partnerships with best-of-breed third party providers.

At Meniga, we are working on PSD2 readiness with our customers around the world — and the first step is to build a personal data innovation platform that enables banks to comply with PSD2 without overloading core-banking systems while at the same time building the foundations on which they can compete with agile FinTechs. For most banks, PSD2 compliance is a significant investment — Meniga helps make this investment count towards compliance as well as enhanced competitiveness.

Opportunity 2: Be a first-mover with “post-PSD2“ products & services

PSD2 is regulating access to data and this will increase demand for data-driven, personalised services & customer experiences. Banks are in an excellent position to take the lead prior to PSD2 by developing data-driven “post-PSD2” products and services and capturing first-mover advantage.

This year we have seen a number of interesting moves as banks step up their game. At Meniga we feel a sense of urgency in the market from banks to make pre-emptive moves to test out “post-PSD2” customer experiences & business models. We see a growing demand for white label data-driven banking products & services, such as our account aggregation products.

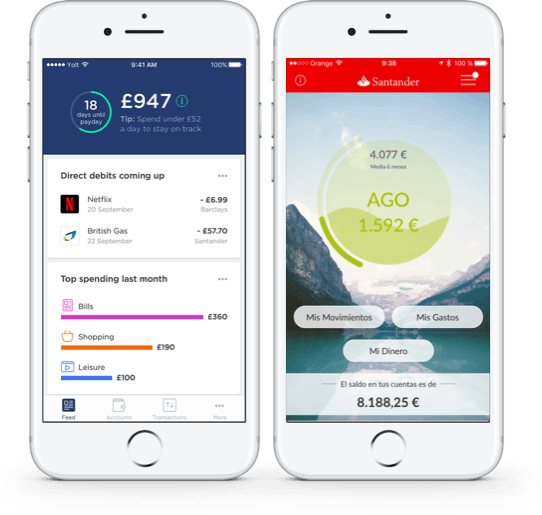

Santander Spain recently launched their MoneyPlan app in Spain, a state-of-the art, notification-driven PFM solution that aggregates financial data to provide a holistic view of people’s finances. ING recently announced the launch of an independently branded PFM solution based on aggregated data in the UK — Yolt. What is perhaps most intriguing about this very public move, is that ING exited the UK market in 2012, when they sold ING direct to Barclays. Is ING using the FinTech momentum as a back-door to re-enter the UK market?

Opportunity 3: Use Data to Expand the Banking Ecosystem

The time has come for banks to start thinking out of the box and define their role more broadly. To date, banks have been hesitant in using their competitive advantages to expand their business model — but with PSD2 around the corner, the time to move is now.

Card Linked Offers are an excellent example of how banks can use data to develop a compelling proposition to personal and corporate clients at the same time. Using transaction data to source compelling offers tailored to each customer’s spending profile — granting merchant access to valuable customer segments and serving the personal banking customers relevant offers in the context of everyday banking. Bank of America was a first mover in this space in the US and many of the major UK banks are now pursuing this as well, including Lloyds and Santander. Once PSD2 is enforced, third parties will be able to launch targeted offer services — but in the meantime banks have a head start.

This is the one area where banks can really take the fight back to what in the end might become the biggest disruptors in financial services — Google and Facebook. As McKinsey noted in their last Global Banking Annual Review, this type of business model innovation has the potential to “change the playing field for banks, vaulting them from incumbents in a $3-trillion to industry to attackers in a $24-trillion one”. It is a big fruit, but not necessarily low-hanging. It takes effective execution to succeed: High data quality, advanced segmentation algorithms and vigorous focus on quality over quantity of campaigns is key to making card-linked offers a truly targeted experience and delivering sustainable value to merchants and consumers at the same time.

Meniga has been operating a B2C Card-Linked Offer program in Iceland delivering compelling commercial and user experience metrics that demonstrate that successfully executed targeted offer programs can drive effective customer engagement and satisfaction while delivering a substantial new revenue stream for banks.

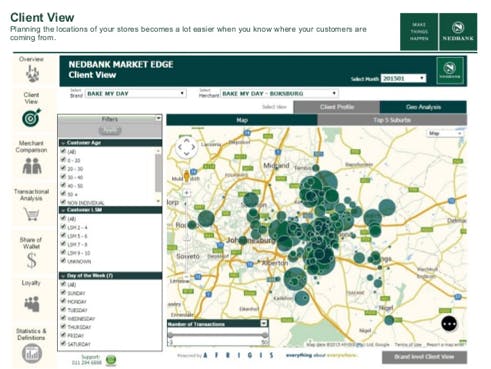

Another example of how banks can use data to build new products and revenue streams is transaction based market intelligence. Banks with reasonable market share have the ability to supply their corporate customers with real-time market share data & store level analysis — a unique strategic marketing tool.

Nedbank launched their MarketEdge market intelligence platform in South Africa last year and are marketing this towards their corporate customer base. At Meniga we have been operating a similar platform in Iceland and we have experienced first hand how valuable such a product can be for merchants.

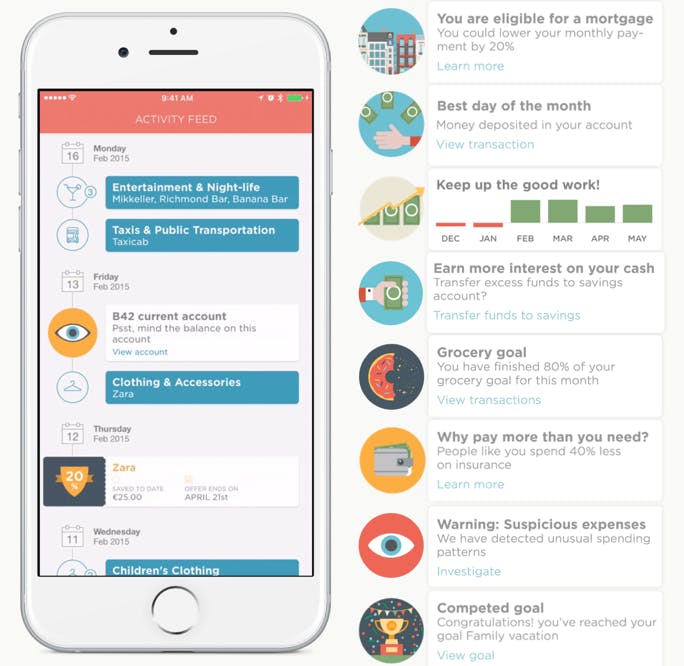

What does Great Digital Banking look like?

When it comes to personal banking — banks have an excellent opportunity to stay relevant in a fast moving mobile world. We spend so much time staring into our mobile devices and arguably a lot of that time is not necessarily well spent. The average global Facebook & Snapchat user spends >20 minutes every day engaging with its apps. Successful mobile games like Pokemon Go are occupying a significant part of people’s attention daily. Is this time well spent?

Here banks are uniquely positioned in the sense that they have the data and insight to build engagement that is addictive and meaningful at the same time: by combining core banking functions with tailored, impartial financial advice, playful notifications and targeted offers from the bank & 3rd parties — banks can dramatically increase customer touch-points by giving them a reason to check in regularly for advice, insights and offers — helping people improve their economies and enrich their lives.